CSRD Explained: Incorporating Double Materiality in EU Corporate Sustainability Assessments

The CSRD is an EU regulation that expands the Non-Financial Reporting Directive (NFRD). It mandates a more detailed reporting of sustainability-related information, aiming to enhance the comparability and reliability of sustainability data reported by companies operating within the EU. The implementation of CSRD is phased, learn more about which companies are subject to it here.

With the introduction of CSRD and therefore standardized sustainability reporting, investors, consumers, and other stakeholders can assess and compare the ESG performance of companies.

A foundational concept of CSRD is double materiality, extending the concept of materiality to include both financial information and the company's impacts on society and the environment.

"Double materiality highlights the interconnectedness of financial performance and sustainability. It pushes companies to be even more accountable for their impact on the world." Alexandra Morton, Founder & MD, circularity.

Under the CSRD compliance, companies are required to conduct double materiality analysis. This analysis compels companies to identify and assess their positive and negative impacts on the environment and society by considering both potential and actual effects. External influences that could affect financial performance must also be included.

ESRS: Structuring ESG Reporting for Consistency and Clarity in EU Industries

To ensure that all relevant ESG information is reported in a consistent, structured manner across all industries within the EU, the European Sustainability Reporting Standards (ESRS) were developed. While CSRD dictates the 'what' of sustainability reporting, ESRS provides the 'how.'

The ESRS provides an overarching framework for all affected company types and sizes. It consists of two cross-cutting standards (ESRS 1 and ESRS 2) and 10 topic-specific standards that cover the so-called Environmental, Social, and Governance issues (ESG).

- ESRS 1 (General Requirements) sets general rules for reporting

- ESRS 2 (General Disclosures) describes basic information that must be published

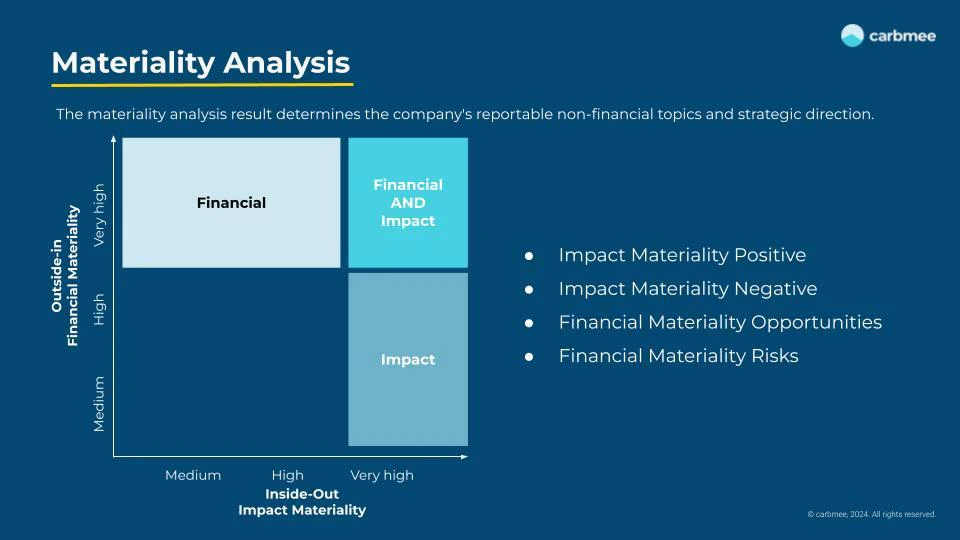

- Topical Standards, depend on the result of the double materiality analysis, considering

Inside-Out perspective (Impact Materiality

Outside-In perspective (Financial Materiality)

These two perspectives are fundamental for identifying strategically relevant sustainability topics and the associated reporting obligations. While each company has to assess which topics are material, almost with certainty ESRS E1 (climate change reporting) and ESRS S1 (own workforce reporting) are material.

The data points for ESRS S1 are not too complex, usually handled in HR systems and fairly easy to report. In contrast, compliant reporting and understanding ESRS E1 pose a significant challenge for companies, due to the complexity of relevant data and a lack of existing systems and processes.

ESRS E1 - addressing Climate Change Disclosures and Strategic Alignment

With its focus on climate change-related disclosures, for ESRS E 1 companies must report their emissions and how their business strategies align with global targets defined in the Paris Agreement.

Requirements

Data Collection: ESRS E1 consists of 220 specific data points. The required data points range from direct emissions to indirect impacts through the value chain, covering Scope 1, 2, and 3. To handle the vast amount of data efficiently and to ensure data accuracy it is almost mandatory to implement carbon data management systems.

Opportunities:

“ When it comes to data, do you want to achieve improvements, or do you want to report the same performance which you reported last year? It comes down to the ability to drill down opportunities. With an emission breakdown, you can access different data points and really make root cause-based decisions on a granular level." Christian Heinrich, Founder & MD, carbmee.

1. Data Analysis: Analyze this data to not only report but also to understand where significant environmental impacts occur and where improvements can be made.

2. Integration of Sustainable Practices: Incorporate sustainable practices into the business strategy to mitigate identified risks and capitalize on new opportunities within a low-carbon economy.

3. Regular Review and Update: Regularly review reporting processes and outcomes to ensure continuous improvement and compliance with evolving standards.

The role of carbon management software for CSDR and ESRS E1

Navigating the complexities of CSRD and ESRS E1 requires a robust strategy backed by powerful tools. With its comprehensive features designed to address the nuances of these new regulations, Carbmee’s EIS platform stands out as an essential ally for companies aiming to meet their sustainability reporting obligations while fostering a sustainable business model.

As regulations evolve and the importance of ESG considerations grows, ensuring compliance with CSRD will not only meet regulatory requirements but also enhance corporate reputation and stakeholder trust.

Simplifiy CSRD reporting and build a lasting legacy with carbmee EIS™